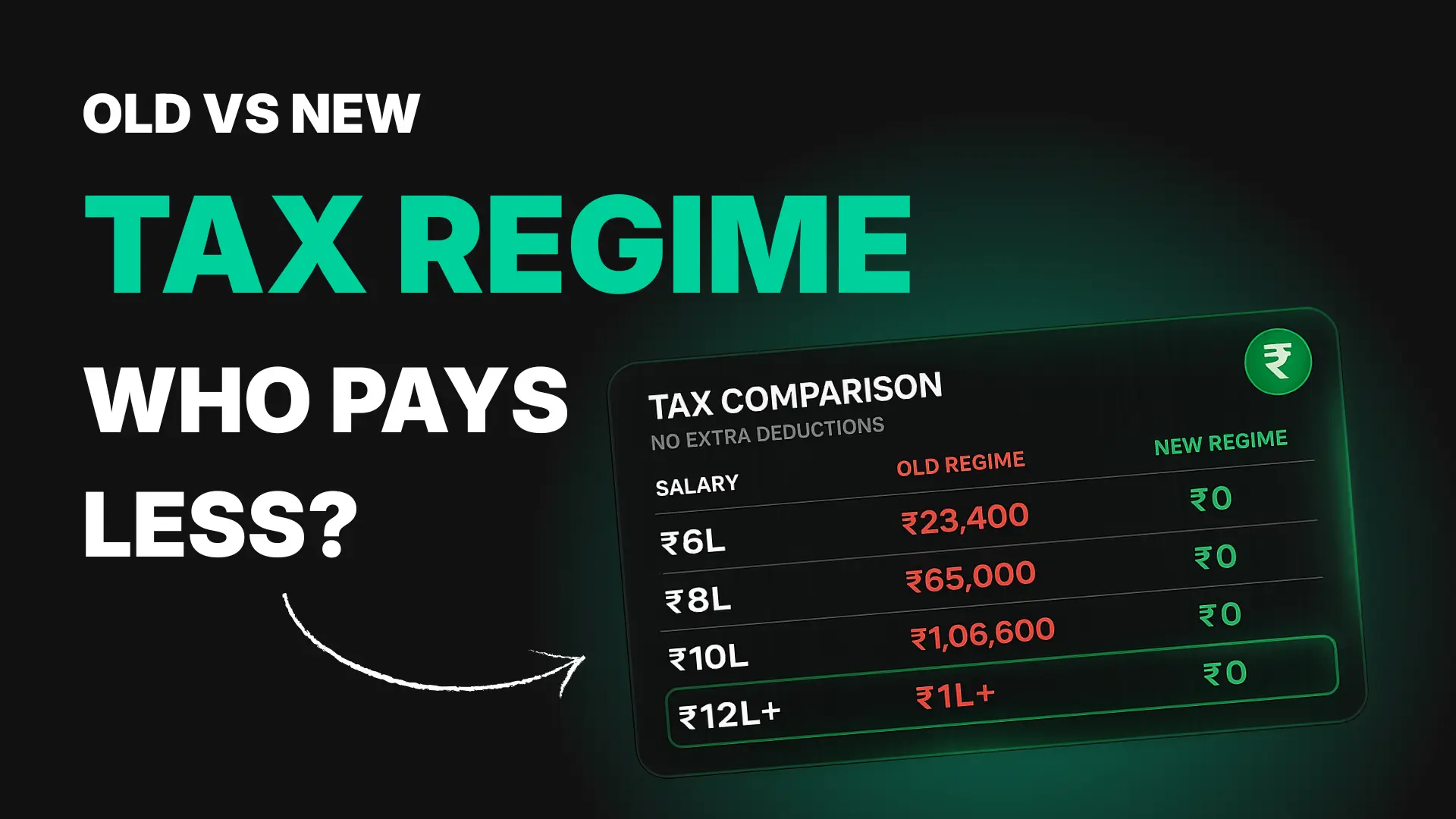

Old vs New Tax Regime 2026: I Ran the Numbers for ₹6L, ₹8L, ₹10L, ₹12L Salary

I compared old vs new tax regime 2026 for ₹6L, ₹8L, ₹10L and ₹12L salary. The truth is simple: new regime gives ₹0 tax up to ₹12.75L gross salary for regular salaried income.

April salary month is dangerous.

HR asks for your tax regime declaration. Friends start saying "old regime is better because 80C." Finance YouTube starts shouting about zero tax. Then you open your payslip and wonder one simple thing: bhai, for my salary, which one actually saves money?

So I ran the numbers myself for four salaries people search the most: ₹6 lakh, ₹8 lakh, ₹10 lakh and ₹12 lakh. I used the official new-regime slabs, old-regime slabs, standard deductions, rebate rules, and 4% cess.

Key Takeaways

- The new regime gives ₹0 tax up to ₹12.75L gross salary for regular salaried income because of the ₹75,000 standard deduction and ₹12L rebate limit.

- At ₹6L, ₹8L, ₹10L and ₹12L salary, new regime wins or ties in the clean comparison.

- Old regime only matches the new regime if your deductions are large enough to pull taxable income down to ₹5L or below.

I am not a CA. I am a digital marketing guy from Panipat who hates vague money advice. When I see "old is better" or "new is better" without a table, my brain treats it like a broken landing page. Show me the numbers, then we can talk.

Use my Income Tax Calculator FY 2026-27 after reading this. The article gives the logic. The calculator lets you test HRA, side hustle income, 80C, NPS, and other deductions on your own numbers.

What Changed in the New Tax Regime for 2026?

The Income Tax Department's Budget 2026 FAQ lists new-regime slabs from 0% up to ₹4L, then 5%, 10%, 15%, 20%, 25%, and 30% above ₹24L (Income Tax Department, 2026). For salaried people, the big deal is the ₹75,000 standard deduction and rebate up to ₹12L taxable income.

That means the new regime is no longer just "simple." For middle-income salaried people, it is brutally competitive.

Here is the new-regime slab structure I used:

| Taxable income under new regime | Tax rate |

|---|---|

| Up to ₹4,00,000 | 0% |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

The twist is Section 87A rebate. If your regular taxable income is up to ₹12L under the new regime, the slab tax gets rebated. For a salaried person, ₹12.75L gross salary can become ₹12L taxable income after the ₹75,000 standard deduction.

According to the Income Tax Department's 2026 Budget FAQ, salaried taxpayers can get the standard deduction in the new regime and still use the rebate threshold up to ₹12L taxable income. In plain English, regular salary up to ₹12.75L can become zero-tax under the new regime, before special-rate income complications.

What Assumptions Did I Use for the Salary Comparison?

The Income Tax Department tax-rate page keeps the old regime slabs at 0% up to ₹2.5L, 5% to ₹5L, 20% to ₹10L, and 30% above ₹10L for individuals below 60 (Income Tax Department, 2026). I used that old-regime slab system with the ₹50,000 salary standard deduction.

My base case is intentionally clean:

| Assumption | Value used |

|---|---|

| Person | Resident salaried individual below 60 |

| Income type | Regular salary only |

| Old-regime standard deduction | ₹50,000 |

| New-regime standard deduction | ₹75,000 |

| Extra old-regime deductions | ₹0 in the first comparison |

| Cess | 4% |

| Surcharge | Not applicable at these salaries |

Why no HRA and 80C in the first table? Because that is the only honest way to see the raw difference.

After that, I added a second table showing how much old-regime deduction you need just to match the new regime. That matters more than a generic "old vs new" answer.

The real question is not "old or new?" The real question is: how much forced deduction do you need before the old regime stops charging tax? At these salary levels, the new regime starts at zero. Old regime has to fight its way down to zero.

Old vs New Tax Regime 2026: What Is the Direct Result?

The new regime gives zero tax for all four salaries in this test because ₹6L, ₹8L, ₹10L and ₹12L gross salary become taxable income below ₹12L after the ₹75,000 standard deduction (Income Tax Department, 2026). Without extra deductions, the old regime charges tax from ₹6L onward.

Here is the table I wanted someone to show me in one place:

| Gross salary | Old regime tax with only ₹50k standard deduction | New regime tax with ₹75k standard deduction | Better option |

|---|---|---|---|

| ₹6,00,000 | ₹23,400 | ₹0 | New regime |

| ₹8,00,000 | ₹65,000 | ₹0 | New regime |

| ₹10,00,000 | ₹1,06,600 | ₹0 | New regime |

| ₹12,00,000 | ₹1,63,800 | ₹0 | New regime |

Source: Author calculation using Income Tax Department old and new regime slabs, 2026.

Source: Author calculation using Income Tax Department old and new regime slabs, 2026.

This is the part most social media posts hide. They compare new regime against an old regime stuffed with every possible deduction. That can be useful, but it is not a beginner's real starting point.

If you don't pay rent, don't have a home loan, don't max NPS, or don't invest ₹1.5L under 80C, the old regime usually looks much weaker.

How Much Tax Do You Pay on ₹6 Lakh Salary in 2026?

At ₹6L gross salary, the new regime tax is ₹0 because taxable salary becomes ₹5.25L after the ₹75,000 standard deduction and stays inside the ₹12L rebate limit (Income Tax Department, 2026). The old regime becomes ₹23,400 if you claim only the ₹50,000 standard deduction.

The old-regime math is simple:

| Step | Amount |

|---|---|

| Gross salary | ₹6,00,000 |

| Less old-regime standard deduction | ₹50,000 |

| Old-regime taxable income | ₹5,50,000 |

| Slab tax before cess | ₹22,500 |

| Add 4% cess | ₹900 |

| Old-regime tax payable | ₹23,400 |

New regime:

| Step | Amount |

|---|---|

| Gross salary | ₹6,00,000 |

| Less new-regime standard deduction | ₹75,000 |

| New-regime taxable income | ₹5,25,000 |

| Tax after 87A rebate | ₹0 |

For ₹6L salary, old regime is not dead. You need just ₹50,000 of extra deduction beyond the standard deduction to bring old-regime taxable income to ₹5L. One decent 80C investment can do that.

But here is the practical point: if the new regime is already ₹0, don't buy a bad insurance policy just to make the old regime also ₹0. Saving tax by buying junk is still junk.

How Much Tax Do You Pay on ₹8 Lakh Salary in 2026?

At ₹8L gross salary, the new regime tax is ₹0 because taxable salary becomes ₹7.25L after the ₹75,000 standard deduction and remains under the ₹12L rebate threshold (Income Tax Department, 2026). Old regime tax is ₹65,000 if you claim no extra deduction.

Old-regime math:

| Step | Amount |

|---|---|

| Gross salary | ₹8,00,000 |

| Less old-regime standard deduction | ₹50,000 |

| Old-regime taxable income | ₹7,50,000 |

| Slab tax before cess | ₹62,500 |

| Add 4% cess | ₹2,500 |

| Old-regime tax payable | ₹65,000 |

To make old regime match the new regime at ₹8L salary, you need extra deductions of about ₹2.5L beyond the ₹50,000 standard deduction.

That usually means maxing ₹1.5L under 80C and finding another ₹1L through HRA, health insurance, NPS, education loan interest, or home loan interest. Possible? Yes. Common for a young salaried person in Panipat, Sonipat, Jaipur, Indore, or a similar city? Not always. For long term planning, you might also want to read my NPS vs PPF 2026 tax saving comparison for a detailed breakdown.

According to the official old-regime slab structure, ₹7.5L taxable income crosses the ₹5L rebate limit, so the old regime cannot use 87A to wipe the bill out (Income Tax Department, 2026). At ₹8L salary, the old regime needs real deductions before it can even tie with the new regime.

How Much Tax Do You Pay on ₹10 Lakh Salary in 2026?

At ₹10L gross salary, the new regime tax is still ₹0 because taxable salary becomes ₹9.25L after the ₹75,000 standard deduction, which remains below ₹12L (Income Tax Department, 2026). In the old regime, the no-extra-deduction tax comes to ₹1,06,600.

Old-regime math:

| Step | Amount |

|---|---|

| Gross salary | ₹10,00,000 |

| Less old-regime standard deduction | ₹50,000 |

| Old-regime taxable income | ₹9,50,000 |

| Slab tax before cess | ₹1,02,500 |

| Add 4% cess | ₹4,100 |

| Old-regime tax payable | ₹1,06,600 |

This is where the old regime starts feeling heavy.

To make old regime also become zero, you need extra deductions of ₹4.5L beyond the standard deduction. That is not just 80C. That is 80C plus NPS plus serious HRA or home loan interest.

My takeaway after running the sheet: ₹10L salary is the danger zone for fake confidence. Many people think "I invest in ELSS, so old regime is better." But ₹1.5L of 80C alone does not make old regime better here. It only reduces old taxable income from ₹9.5L to ₹8L.

If you are on ₹10L salary and your old-regime deductions are only 80C, the new regime is still cleaner. You can still invest for wealth, of course. I wrote about beginner mutual fund choices here: best mutual funds for beginners in India.

How Much Tax Do You Pay on ₹12 Lakh Salary in 2026?

At ₹12L gross salary, the new regime tax is ₹0 because taxable salary becomes ₹11.25L after the ₹75,000 standard deduction and stays below the ₹12L rebate threshold (Income Tax Department, 2026). Old regime tax becomes ₹1,63,800 without extra deductions.

Old-regime math:

| Step | Amount |

|---|---|

| Gross salary | ₹12,00,000 |

| Less old-regime standard deduction | ₹50,000 |

| Old-regime taxable income | ₹11,50,000 |

| Slab tax before cess | ₹1,57,500 |

| Add 4% cess | ₹6,300 |

| Old-regime tax payable | ₹1,63,800 |

At ₹12L salary, old regime needs ₹6.5L of extra deductions to reach zero tax. For most salaried people, that is a lot.

You may reach it if you have high HRA in a metro, ₹1.5L 80C, ₹50,000 NPS, health insurance, and maybe home loan interest. But if you live with parents, have no rent, and only do small SIPs, old regime will not magically help.

The new regime's ₹12L taxable-income rebate is the reason this result looks surprising. It does not mean every ₹12L person should stop investing. It means investments should be chosen for goals, liquidity, risk, and returns, not only for tax proof collection.

When Can the Old Regime Still Make Sense?

The old regime can still make sense when deductions are large enough to beat the new-regime tax, especially above the ₹12.75L gross salary zone where the new-regime rebate stops (Income Tax Department, 2026). For these four salaries, old regime mainly tries to match zero, not beat it.

Here is the real break-even table:

| Gross salary | Extra old-regime deductions needed to make tax ₹0 | What that means |

|---|---|---|

| ₹6L | ₹50,000 | Easy with 80C |

| ₹8L | ₹2,50,000 | Needs 80C plus something else |

| ₹10L | ₹4,50,000 | Needs serious HRA or home loan support |

| ₹12L | ₹6,50,000 | Hard for most non-metro young earners |

This table is the whole truth. If your extra deductions are below these numbers, new regime wins. If your extra deductions meet these numbers, old regime can match. It still may not be worth the paperwork unless those expenses or investments already make sense for your life.

Here is how I would decide:

| Your situation | Likely better choice |

|---|---|

| No rent, no home loan, low 80C | New regime |

| Living with parents and investing small SIPs | New regime |

| High metro rent with HRA | Calculate both |

| Home loan interest plus full 80C | Calculate both |

| Salary above ₹12.75L | Calculate both carefully |

Do not use "old regime" as an excuse to buy random endowment plans in March. Tax saving is useful. Locking money for poor returns is not.

What Should You Tell HR in April 2026?

The Income Tax Department's salaried-individual guidance says the new tax regime is the default regime, while eligible taxpayers can choose the old regime subject to rules and timelines (Income Tax e-Filing, 2026). Your employer declaration mainly affects TDS during the year.

If your salary is ₹6L, ₹8L, ₹10L or ₹12L and you don't have heavy old-regime deductions, declaring the new regime to HR is usually the clean option.

My practical April checklist:

- Open your latest CTC or salary structure.

- Separate actual gross salary from employer PF and variable bonus.

- Add side hustle or freelance income if you have it.

- Put the numbers into the MonuMoney income tax calculator.

- Add HRA, 80C, NPS, 80D, education loan interest, and home loan interest.

- Choose the regime with lower yearly tax.

- Save a screenshot or PDF for your records.

If you run a side hustle, be extra careful. Salary plus freelance income can push your total above the rebate zone. I have a separate guide on income ideas here: side hustles in India for 2026.

Also remember the difference between HR declaration and ITR filing. HR uses your declaration to deduct TDS monthly. Your final tax gets settled when you file the return. Don't ignore the monthly TDS impact, though. Cash flow matters.

Frequently Asked Questions

The new regime uses a ₹75,000 standard deduction for salaried taxpayers and rebate up to ₹12L taxable income, while the old regime keeps the ₹5L rebate threshold for normal income (Income Tax Department, 2026). These FAQs answer the salary questions people usually ask before choosing a regime.

Is ₹12 lakh salary tax-free in the new regime in 2026?

Yes, for regular salaried income, ₹12L gross salary can be tax-free under the new regime. After the ₹75,000 standard deduction, taxable income becomes ₹11.25L, which stays below the ₹12L rebate threshold listed by the Income Tax Department in its 2026 Budget FAQ.Which tax regime is better for ₹8 lakh salary?

For ₹8L salary, the new regime gives ₹0 tax in this calculation because taxable income becomes ₹7.25L after standard deduction. Old regime tax is ₹65,000 if you claim only the ₹50,000 standard deduction. Old regime needs around ₹2.5L extra deductions to match zero.Can old regime beat new regime at ₹10 lakh salary?

At ₹10L salary, the new regime tax is ₹0 because taxable income becomes ₹9.25L. Old regime can only match zero if extra deductions pull taxable income from ₹9.5L to ₹5L, meaning about ₹4.5L deductions beyond the standard deduction.Does 80C make the old regime better automatically?

No. 80C has a ₹1.5L limit, but the deduction needed to make old regime tax-free is ₹2.5L at ₹8L salary, ₹4.5L at ₹10L salary, and ₹6.5L at ₹12L salary. 80C alone is often not enough.Can I change tax regime while filing ITR?

Salaried taxpayers without business income generally get more flexibility than business taxpayers, but your HR declaration decides monthly TDS. The new regime is the default regime according to the Income Tax e-Filing portal guidance, so calculate before declaring and again before filing.Final Verdict

For ₹6L to ₹12L salary, the new regime gives ₹0 tax in this clean comparison because the ₹75,000 standard deduction keeps taxable salary under the ₹12L rebate threshold (Income Tax Department, 2026). The old regime only becomes equal when deductions are strong enough.

My honest answer:

- ₹6L salary: new regime is simpler, old can match with small deductions.

- ₹8L salary: new regime wins unless you have around ₹2.5L deductions.

- ₹10L salary: new regime wins for most young salaried people.

- ₹12L salary: new regime is surprisingly strong because tax still becomes ₹0.

Don't choose a tax regime by vibes. Put your exact salary, HRA, rent, 80C, NPS, health insurance, and side income into the free income tax calculator. Five minutes now can save a year of wrong TDS.

Disclaimer: I am not a Chartered Accountant. This article is for education and personal finance awareness only. Tax rules can vary based on salary structure, special-rate income, deductions, and filing status. Please verify with a qualified CA before filing your return.

Official Sources & Verification

To ensure accuracy, the formulas, rules, and tax provisions used on this page are verified against official government, regulatory, or institutional sources.

- Income Tax Department of India

- Union Budget & Finance Bill

- Reserve Bank of India (RBI)

- Securities and Exchange Board of India (SEBI)

Last Verified: April 24, 2026