My ₹35,000 Salary Budget Sheet — How I Track Every Rupee in India 2026

A B.Tech CSE guy from Panipat on ₹35k/month take-home. 57% savings rate. No personal finance guru fluff. Just my actual sheet you can copy in 2 minutes.

Let me start with the embarrassing truth.

In December 2025, I had ₹35,000 hitting my bank account every month and I could not tell you — to save my life — where it was going. Chai runs. One Swiggy order. A random kurta for Diwali. A bike servicing I somehow forgot about until the mechanic called. ₹500 here. ₹800 there. By the 25th of every month I was checking UPI balance before ordering anything.

And this is with me living at home in Panipat, with zero rent, zero EMI on a house, and my mom feeding me every day.

If I couldn't manage ₹35k in that setup, how were people managing in Mumbai or Bangalore on the same salary with ₹18k rent?

That question kicked off the entire budgeting experiment I'm going to show you.

What This Post Actually Is

This is not a "50/30/20 rule" post. I tried that. It broke within 3 days.

This is not a "download this complicated Excel with 47 tabs" post either. I tried those too. Abandoned by day 5.

This is the exact budget sheet I built in January 2026 — after failing with two app-based systems and one notebook system — that I've actually used for 4 consecutive months now. I'm sharing my real numbers. I built the Excel file myself using my CSE background and vibe coding. It's free to download at the end of this post.

My take-home: ₹35,000/month. My savings + investing rate: 57%. My rent: ₹0 (I live at home — more on why I'm honest about this below).

Here's everything.

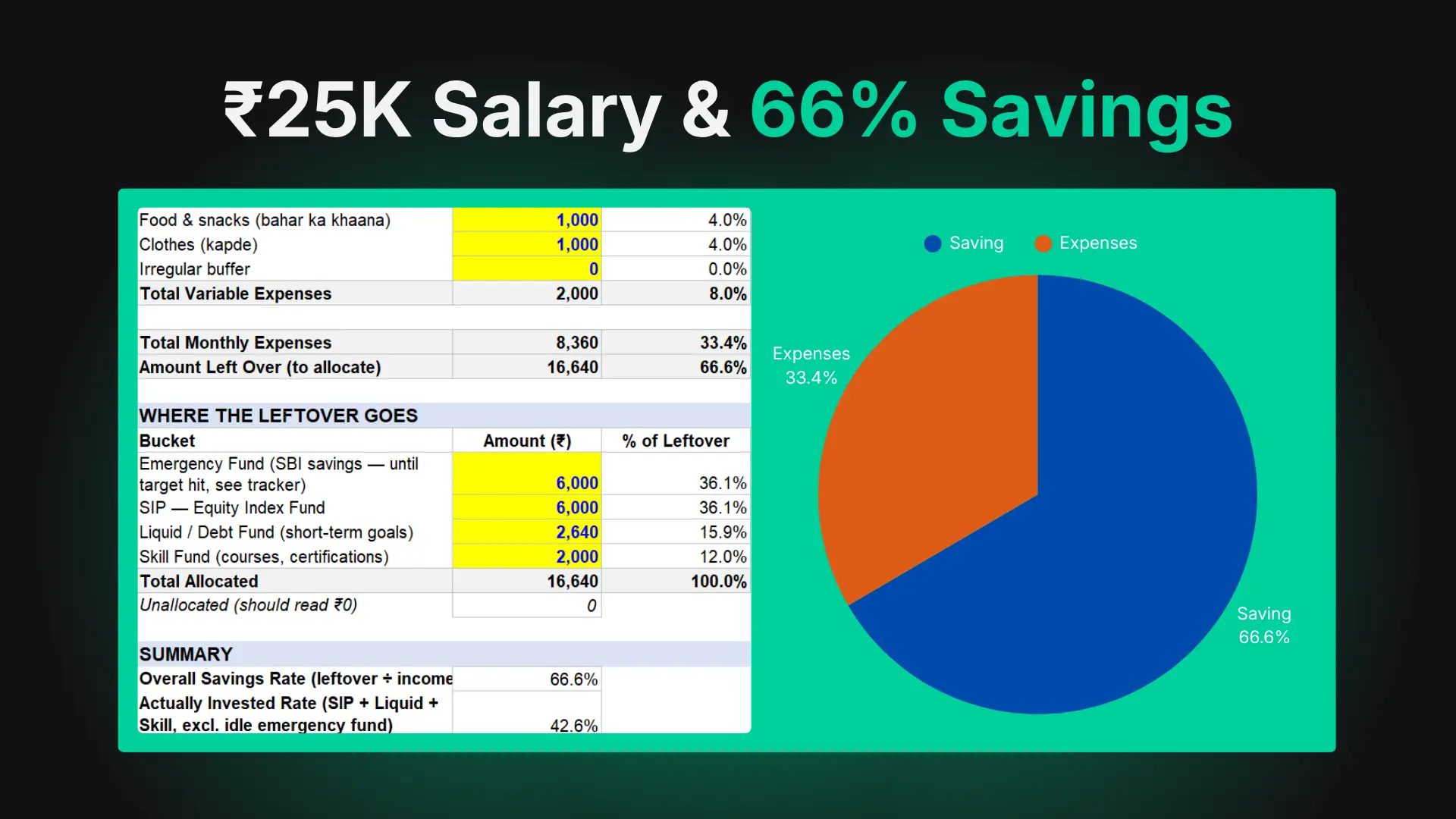

If you're earning less than this right now: two posts cover the earlier chapters. I cleared ₹15,000 of credit card debt on a ₹25,000 salary using the snowball method — that grind is documented here. And after the debt was gone, I was still on ₹25,000 and saving 66% of it — a higher savings rate than the one in this post — while getting it completely wrong, because almost all of it sat in a savings account earning 2.5%. That breakdown is here. Read that one first if ₹35,000 feels far away.

Why My First Three Budget Attempts Failed

Before the sheet, I want you to see the failures. Because if you've also failed at budgeting in India, it's not because you're bad with money. It's because most systems are built for Americans with very different lives.

Attempt 1 — Walnut / Money Manager App (failed in 4 days): The app auto-categorized my UPI transactions. Sounds great. Except: my ₹10,000 transfer to mom got categorized as "friends and family." My Zerodha investment showed up as "shopping." My monthly phone recharge looked like an entertainment expense. I spent 20 minutes every evening re-categorizing. Quit.

Attempt 2 — 50/30/20 Rule (failed by day 3): The rule says 50% needs, 30% wants, 20% savings. On ₹35k that's ₹17,500 needs, ₹10,500 wants, ₹7,000 savings. The problem: my actual "needs" in India are maybe ₹13,000 — I live at home, I don't pay rent or EMI. And ₹10,500 on "wants"? That's the entire problem I was trying to solve. The rule made no sense for my life.

Attempt 3 — Notebook + Pen (failed by day 12): I tracked every expense in a small notebook. Day 1 to 11 — solid. Day 12 — left the notebook at home. Day 13 — forgot to write ₹40 chai. Day 14 — forgot to write ₹280 Swiggy. By day 20 my notebook was a lie, and I knew it.

The lesson from three failures: a budget system only works if it is built specifically for your life, runs automatically on calculation, and requires 5 minutes a month, not 20 minutes a day.

So I built that sheet.

How I Think About Money in Buckets (The Mental Model)

Before I show the structure, the mental model matters. I don't think of ₹35,000 as one big number. I think of it as 4 buckets that get filled in this specific order on salary day:

- Income bucket — What actually hits the account

- Fixed bucket — Non-negotiable bills that drain on schedule

- Variable bucket — The stuff I can control (food, shopping, fun)

- Wealth bucket — SIP, stocks, trading, emergency fund

Whatever's left after all four = cushion. In a clean budget, cushion = ₹0. Because if there's leftover unallocated money, it becomes a Swiggy order by the 28th. Every single time.

This order matters. Most people do Income → Fixed → Variable → whatever's left → Wealth. That's why they never save. Reverse it. Pay yourself first, then Swiggy.

The Actual ₹35,000 Breakdown (My Real Numbers)

Here's exactly where my money goes every month. No rounding, no hiding. If you're on a similar salary in a smaller Indian city, this gives you a real benchmark.

Fixed Expenses

| Category | Amount (₹) | Honest Note |

|---|---|---|

| Home contribution (to Mom) | 10,000 | Replaces rent. Includes food, shared utilities, internet. |

| Bike commute (petrol) | 1,500 | Daily office up-down in Panipat on my bike. |

| Phone recharge (Jio) | 365 | One ₹365 plan. That's it. |

| Electricity share | 700 | Average across summer/winter. |

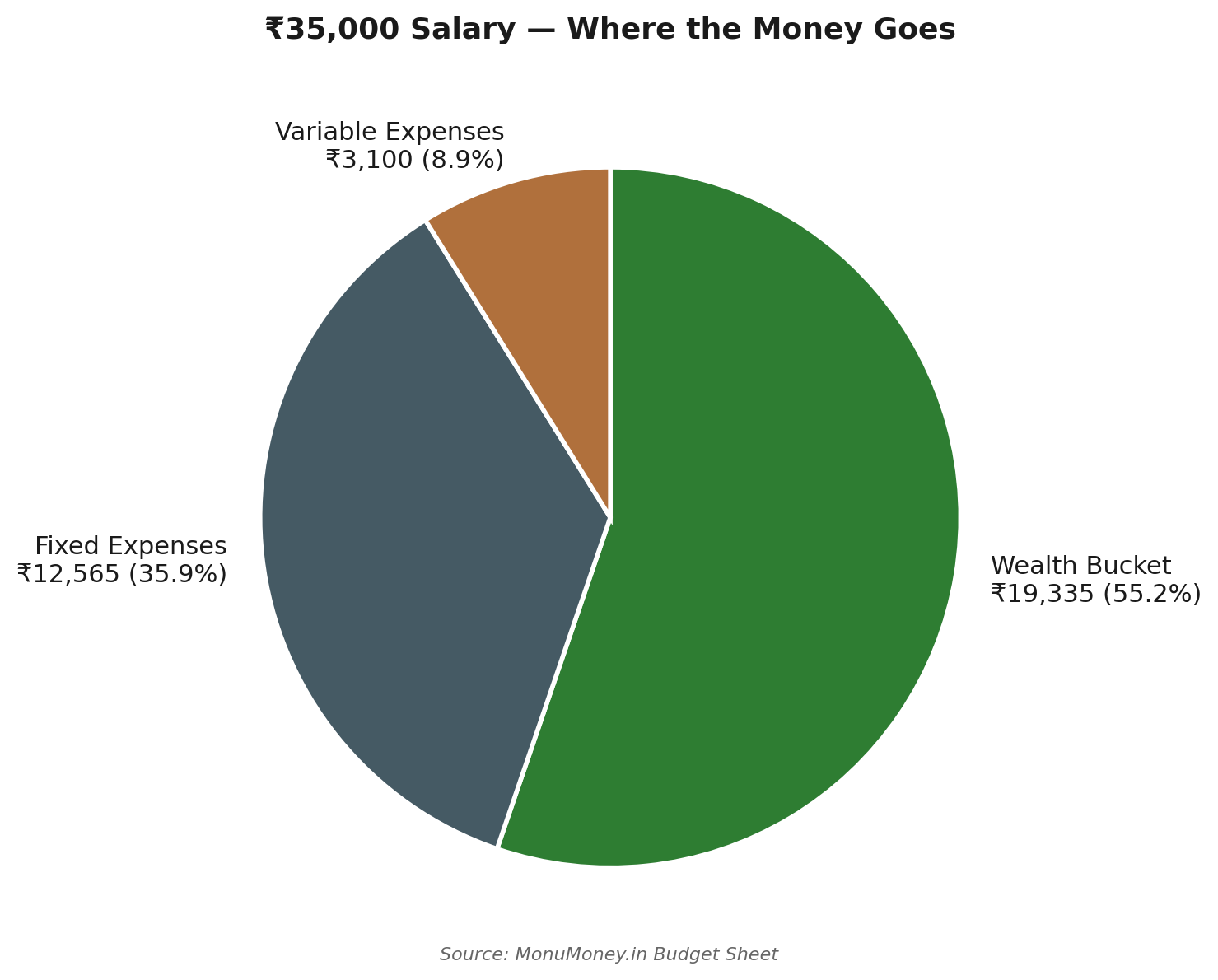

| Total Fixed | 12,565 | 36% of my income |

Important honesty about the ₹10,000 to Mom: A lot of Indian finance blogs skip this category entirely. They pretend people living at home have ₹0 in housing costs. That's a lie. If you live at home and don't contribute — either you're a college student, or you're freeloading and calling it budgeting. I count this as my rent. You should too.

Variable Expenses

| Category | Amount (₹) | Honest Note |

|---|---|---|

| Weekend food, snacks, fast food | 1,600 | ₹300-500/week cravings. Samosa, Zomato, the occasional Domino's. |

| Irregular buffer | 1,500 | Festivals, a friend's birthday, new kurta, bike servicing. Real life happens. |

| Total Variable | 3,100 | 9% of my income |

The ₹1,500 buffer is the single most important line item I added after my three failures. Because "real life" is not a monthly-predictable thing. Some months it's ₹0. Some months a wedding invite wipes out ₹2,200. Averaging it at ₹1,500 means I stop panicking when real life shows up.

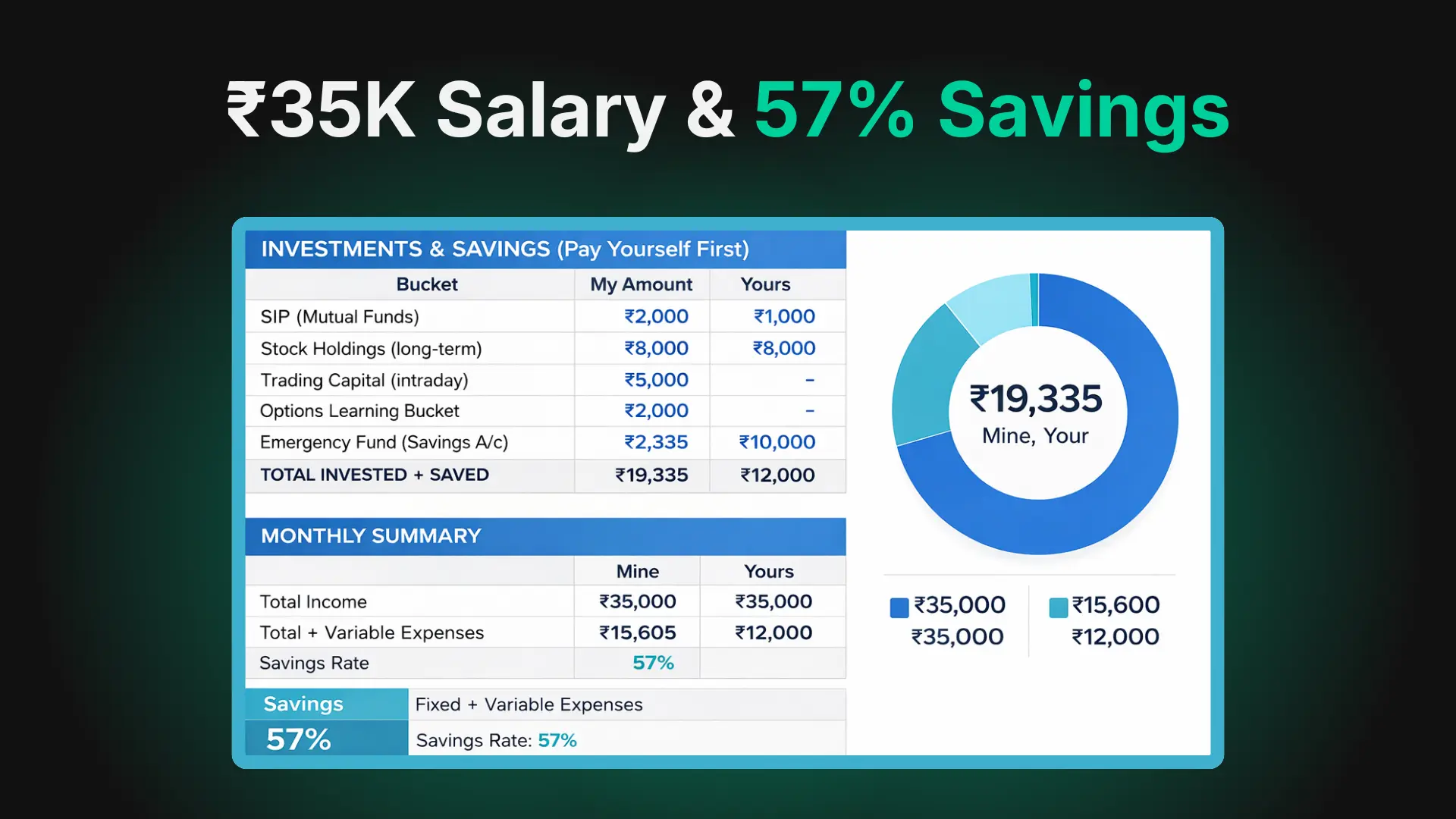

Investments + Savings (The Wealth Bucket)

| Bucket | Amount (₹) | Honest Note |

|---|---|---|

| SIP (Mutual Funds on Groww) | 2,000 | Auto-debit. Index fund. I wrote about my portfolio here. |

| Stock Holdings (Zerodha) | 8,000 | Large-cap buy-and-hold only. Not trading. |

| Trading Capital (intraday) | 5,000 | Kept completely separate. Never risk more than 2% per trade. |

| Options Learning Bucket | 2,000 | Small amount. I'm learning. NOT recommending this to anyone else. |

| Emergency Fund | 2,335 | The leftover goes straight to savings account. Target check: emergency fund calculator. |

| Total Wealth | 19,335 | 55% of my income |

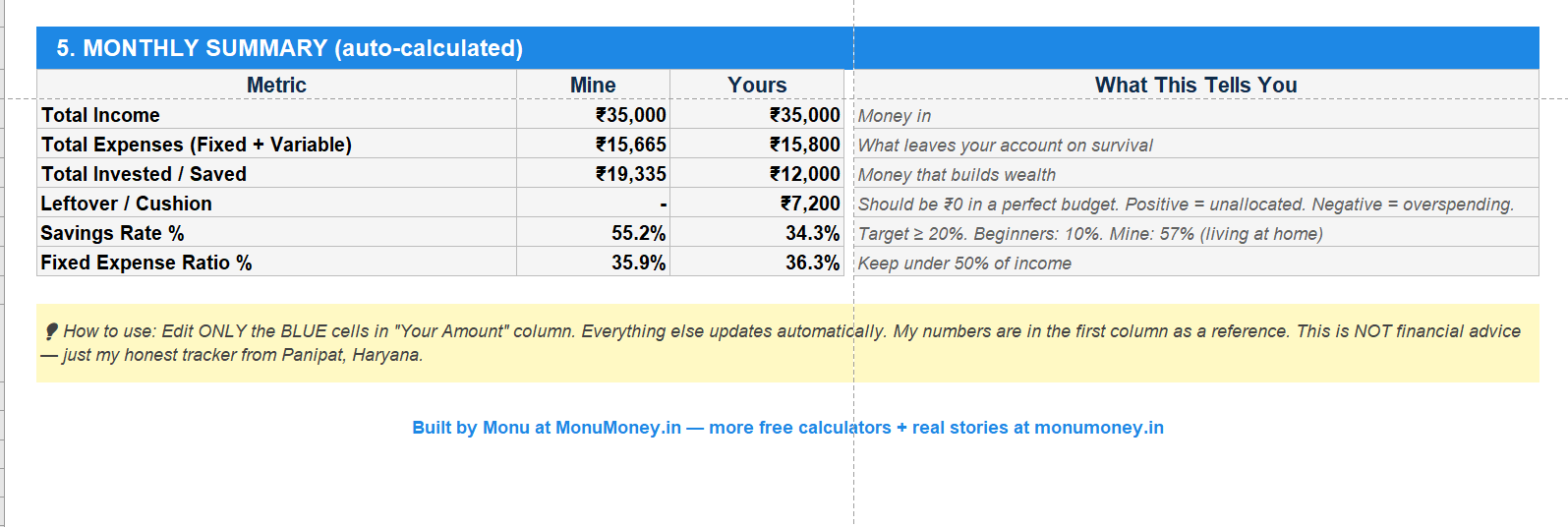

The Monthly Summary

| Line | Amount (₹) |

|---|---|

| Total Income | 35,000 |

| Total Expenses (Fixed + Variable) | 15,665 |

| Total Invested / Saved | 19,335 |

| Cushion (what's unallocated) | ₹0 |

| Savings Rate | 55.2% |

₹0 cushion is not an accident. That's the entire point of the system. Every rupee has a job. If cushion > ₹0, money evaporates. If cushion < ₹0, you're overspending and need to rebalance.

A Critical Honesty Check on My Savings Rate

My 55% savings rate looks incredible on paper. It would look even more incredible on a LinkedIn post. Let me kill that narrative immediately.

My savings rate is high because:

- I live at home. Zero rent. Zero homeowner EMI.

- My mom cooks my daily meals. My weekday food cost is essentially ₹0.

- Panipat is not Mumbai. Everything from haircuts to petrol is cheaper here.

- I'm 22. I have no dependents, no kids, no aging parent I'm paying medical bills for.

- I cleared my ₹15,000 credit card debt before this period started, so I have zero EMI drag.

If I moved to Gurgaon tomorrow for a ₹60k job, I'd lose ₹20k to rent, ₹6-8k to food delivery, ₹3k to extra commute — and my savings rate would probably drop to 25-30% even on higher income.

What this means for you: Do not compare your savings rate to mine. Compare it to your own past months. That's the only benchmark that matters.

And a savings rate on its own tells you very little anyway. On ₹25,000 I hit 66% — higher than this — and it was worse, because the money sat in a savings account instead of an index fund. The full argument for why deployment beats savings rate is here.

The Exact Spreadsheet Structure I Use

Here's how the sheet is organized — in case you want to rebuild it yourself or understand what you're downloading.

Sheet 1 — Budget: Four stacked tables (Income → Fixed → Variable → Wealth), each with a running total. Then a Summary block at the bottom with auto-calculated savings rate, fixed expense ratio, and cushion. Only 2 columns are editable (my numbers stay in one column as a reference, your numbers go in the next). Everything else is formulas.

Sheet 2 — How to Use: 6 steps for first-time setup, plus FAQs I actually get asked.

Sheet 3 — Category Key: Plain-English definitions of every category in Indian context. "Home Contribution" vs "Rent" is explained. "Trading Capital" vs "Stock Holdings" is explained. No ambiguity.

The whole file has 20 working formulas and zero hardcoded totals — change one blue input and everything recalculates.

4 Budgeting Mistakes I See Beginners Make in India

After helping a few friends set up this sheet, these are the mistakes I see on repeat:

Mistake 1 — Not contributing to household and calling yourself a saver. If your parents feed you, house you, and pay your WiFi, and you're "saving" ₹30,000 a month on a ₹35k salary — that's not saving. That's dependency. Contribute honestly. Put a ₹ number on what your parents subsidize. Adjust your savings rate for reality.

Mistake 2 — Treating SIP as optional. "I'll invest whatever is left at month end." There is never anything left at month end. There is never going to be anything left at month end. Set SIP auto-debit for the 2nd of every month — salary day + 1. What you can't see, you can't spend. Run your own numbers on the SIP calculator — even ₹2,000 a month looks different once you see the 20-year figure. And given recent market trends, see my analysis on the record 2026 SIP inflows vs FPI outflows.

Mistake 3 — Treating trading capital as savings. Your intraday / options trading bucket is NOT your emergency fund. It is not your savings. It is risk capital. If you lose ₹5,000 in a bad trade, your emergency fund should be completely untouched. Keep them in different accounts — literally. I have one savings account for emergency, one for trading. Zero overlap. This separation is exactly what let me sit still during the 10% market correction in May 2026 without touching my SIP.

Mistake 4 — Forgetting the irregular buffer. The single biggest reason budgets fail: no line for "real life." A cousin's wedding costs ₹2,000 in gifts. Your bike servicing costs ₹800. Your shoes tear and you need new ones — ₹1,500. These things will happen. Budget for them with a ₹1,000-2,000 monthly buffer. When they don't happen, the buffer becomes extra savings.

What I'd Change If My Salary Hit ₹60,000 Tomorrow

This is the thought experiment I run every few months. If my take-home doubled to ₹60k, what would I do?

- Home contribution: Increase to ₹15,000. My mom's costs have gone up too; inflation is real.

- SIP: ₹2,000 → ₹8,000. Still conservative, but meaningful.

- Stock holdings: ₹8,000 → ₹15,000. Scale the buy-and-hold portfolio.

- Trading capital: Keep at ₹5,000. DO NOT scale trading based on income. Risk management doesn't change.

- Lifestyle upgrade: ₹3,000 more on food and clothes. Human being hai, robot nahi.

- Health insurance: Add ₹1,500 for a proper health cover. Currently I'm on my dad's. That won't last.

- Skill investment: ₹2,000 for a paid course or certification. Quarterly, not monthly.

Total allocated in that scenario: ₹49,500. Remaining ₹10,500 cushion would go to the emergency fund until I hit 6 months of fixed expenses.

Lifestyle inflation is the enemy. If you get a 40% raise and lifestyle eats 40%, you're in the same financial spot, just with a bigger apartment.

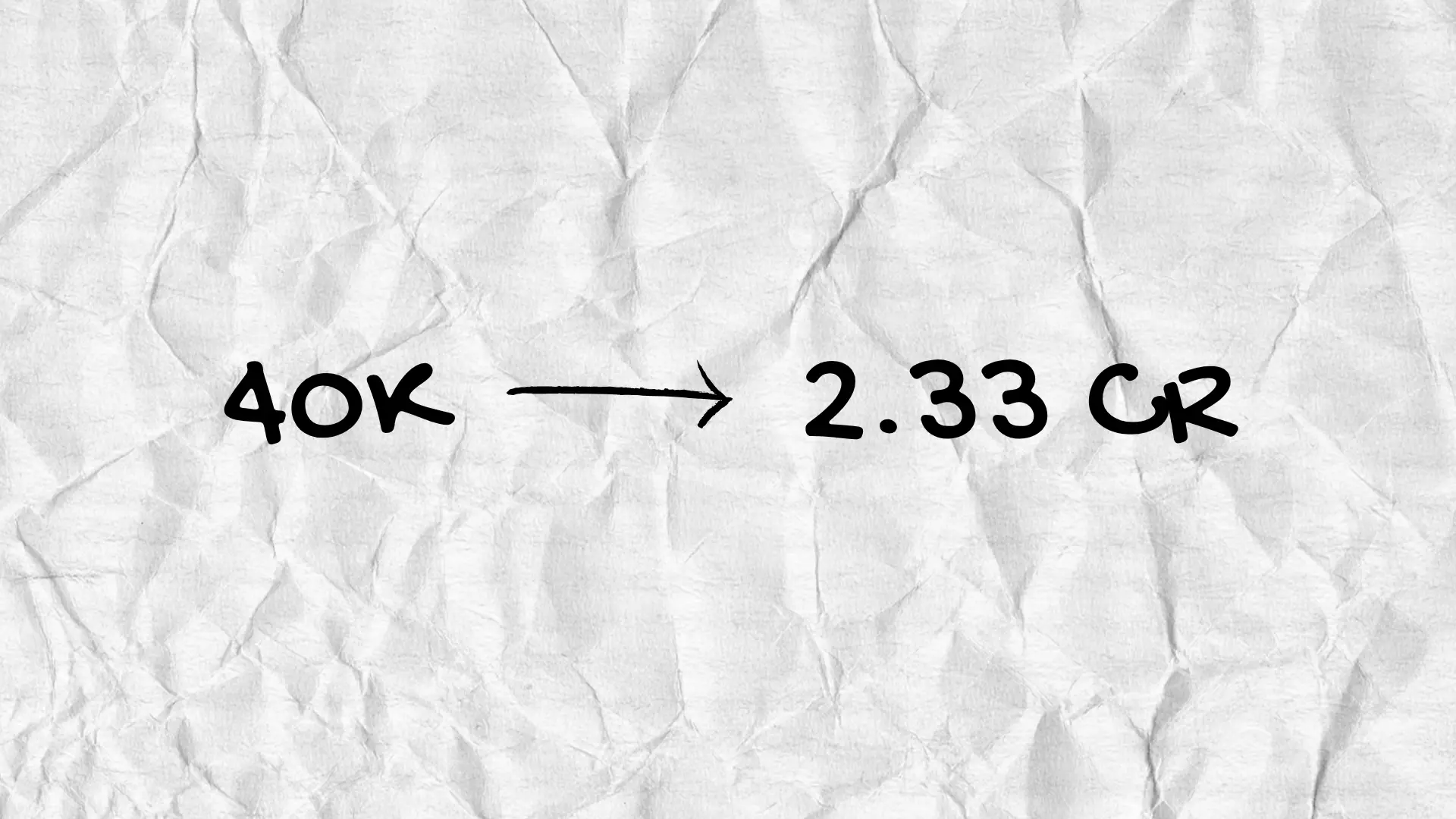

The honest way to scale a SIP alongside a rising salary is a step-up — increasing the amount by a fixed percentage each year instead of leaving it flat. The step-up SIP calculator shows the difference, and it is not small over 15 years. Just be careful about which projections you believe: I took apart a viral ₹40k-salary-to-₹2.33-crore claim here, and the nominal number was technically right while being deeply misleading.

3 Rules I Follow That Made This Sheet Stick

After 4 months of actually using this, these are the rules that keep it alive:

Rule 1 — 5 minutes a month, not 20 minutes a day. I update the sheet once — on the 1st of the month, before work. I look at my bank statement for the previous month, I plug in the actual category numbers, I compare to plan, I adjust. 5 minutes. Done.

Rule 2 — The categories are never perfect. The habit is. Don't try to track 30 categories. You'll quit in a week. My sheet has 14 total categories. That covers 95% of my spending. The last 5% goes into "irregular buffer." Good enough is the correct target.

Rule 3 — If one month is a disaster, that's okay. Two in a row is a problem. April was bad for me — I went to Delhi for a friend's wedding, overspent ₹3,200. Cushion went negative. Instead of panic, I asked: was this a one-off or a pattern? It was one-off. Moved on. Budgeting is a long game. Don't let perfect be the enemy of the habit.

Download the Sheet

Everything I've described above is in a single Excel file. Zero login, zero email gate (for now), zero ads in the file. Click below to download. Open it. Edit the blue cells. Watch the numbers update.

👉 Download MonuMoney_35k_Budget_Sheet.xlsx

My numbers stay visible in one column as a reference. Your numbers go in the next column. The summary updates as you type. If your "Leftover / Cushion" goes red, you're overspending — adjust until it hits ₹0.

Earning less than ₹35,000? There's a ₹25,000 version of this sheet built for freshers, with an emergency fund tracker that tells you when to stop saving and start investing.

Frequently Asked Questions

How much should I save on a ₹35,000 salary in India?

It depends almost entirely on your housing situation, not your discipline. Living at home with no rent, 40-55% is achievable — I manage 55%. Paying ₹12,000-15,000 rent in a metro on the same salary, 15-25% is a realistic target and still good. The useful benchmark is not someone else's percentage; it's whether this month beat last month. Start by tracking one full month before setting any target.Does the 50/30/20 rule work in India?

Poorly, for most people. The rule assumes housing is your largest fixed cost and that "wants" deserve 30% of income — both of which come from an American context. If you live with family, your genuine needs might be 25-35% of income, which makes the 50% needs bucket meaningless. If you pay metro rent, needs alone can exceed 65% and the rule becomes impossible. Build the categories around your actual life instead, and let the percentages fall where they fall.How much should I give my parents if I live at home?

There's no formula, but there is a floor: put a real number on it, even if they refuse the money. I give ₹10,000 out of ₹35,000 — roughly 29% — which covers food, my share of utilities, and internet. When I was on ₹25,000 it was ₹5,000. Two reasons this matters beyond fairness: your savings rate is fiction without it, and you need an accurate baseline for the day you move out and pay market rent.Is a 55% savings rate realistic on ₹35,000?

Only under specific conditions — no rent, no EMI, no dependants, and a tier-2 or tier-3 city cost base. All four apply to me. Remove any one and the number drops sharply. If I moved to Gurgaon on ₹60,000, I'd expect 25-30% despite earning almost double. Treat high savings rates on social media as a description of someone's circumstances, not their discipline.How much emergency fund do I need on a ₹35,000 salary?

Six months of your actual monthly expenses, not six months of salary. My expenses are ₹15,665, so my target is roughly ₹94,000 — not ₹2.1 lakh. Keep it in a plain savings account separate from your salary account, accessible within a day. And treat it as a target with a finish line: once it's full, redirect that entire monthly contribution to your SIP rather than letting it accumulate at 2.5% forever. The emergency fund calculator works out your number.Should I start a SIP before my emergency fund is complete?

Run a small one alongside it. The habit is harder to build than the balance, and people who wait for the "right time" often wait years. Keep the SIP modest — ₹1,000-2,000 — and put the bulk of your surplus into the emergency fund until it's done. Then the emergency fund line ends and that whole amount moves to investing. What you should not do is stop an existing SIP to build the fund faster.What if I pay rent — how does this budget change?

The structure holds; the numbers move. On ₹35,000 with ₹12,000 rent, your fixed bucket lands near 60% instead of my 36%, which leaves roughly ₹8,000-10,000 for the wealth bucket rather than ₹19,335. That's a 25-28% savings rate and it is perfectly respectable. Keep the irregular buffer and the fun-money line intact — those are the two things that keep a tight budget alive past week three.Do I pay income tax on a ₹35,000 salary?

No. ₹35,000 a month is ₹4.2 lakh a year, and under the new tax regime salaried income up to ₹12.75 lakh has zero liability. Which means tax-saving products pitched at you right now — ELSS, tax-saver FDs, insurance-linked plans — solve a problem you don't have, while locking your money for 3-5 years. I explained why I cancelled my own ELSS SIP over exactly this, and the full regime comparison is here.Can I use this sheet on a different salary?

Yes. Change the income cell and adjust the category amounts — every total, ratio and the savings rate recalculate on their own. The structure works from ₹15,000 to ₹1,50,000; only the numbers move. If you're closer to ₹25,000, the ₹25,000 version has categories tuned for a first job.What's Next

When I first published this in April, I promised a dedicated emergency fund post next. That specific post still hasn't happened — but the idea that mattered most from it ended up inside the ₹25,000 budget post: an emergency fund is a target with a finish line, not a habit you feed forever. That was the mistake I made on my first salary, and it cost more than any overspending ever did.

What did get written since: why I cancelled my ELSS SIP, what to do when the market falls 10%, and if the answer to a tight budget is more income rather than more optimisation, five side hustles I actually tried.

If you have questions about the sheet, hit me up on X or LinkedIn or drop a note at contact@monumoney.in. If you find a bug in the sheet — even better, tell me. I'll fix it within 24 hours and credit you in the next update.

This is not financial advice. I am not a CA or SEBI-registered advisor. I am a B.Tech CSE student and digital marketer in Panipat sharing my exact system. Your numbers will differ based on city, dependents, and income. Adjust for your life. Always do your own research.