ITR Filing 2026: 7 New Rules That Quietly Killed The Old Tax Regime

ITR filing 2026 just got a massive overhaul. ₹12L tax-free, new 8-city HRA, ITR-3 deadline Aug 31, 48-month ITR-U. Here's what changed for AY 2026-27.

Bhai, the old tax regime is dead. Most people just don't know it yet.

I'm filing my own ITR this year for the first time as a mix-income earner — salary from my day job as a Digital Marketing Team Lead, plus freelance income from MonuMoney.in. So I went deep into the rules for AY 2026-27. What I found genuinely surprised me.

The Income Tax Department has changed 7 major rules for ITR filing in 2026. Most blogs are recycling the same generic Budget 2025 summary. Nobody is connecting the dots on what these rules actually mean if you're a regular salaried person making ₹6L–₹15L, or a freelancer juggling Section 44ADA presumptive taxation.

This isn't going to be that article.

I cross-checked CBDT notifications on the official Income Tax Department portal, ran the actual math through both regimes for my own salary, and here's the brutal truth: if you're under ₹12.75 lakh of taxable income and you're still planning to file under the old regime, you're probably leaving real money on the table.

Let me explain.

TL;DR: For ITR filing 2026 (AY 2026-27), the Section 87A rebate jumped to ₹60,000 — making ₹12 lakh tax-free under the new regime, ₹12.75 lakh for salaried. Form-specific deadlines now apply (ITR-1/2 by July 31, ITR-3/4 by August 31). HRA 50% exemption expanded to 8 cities. ITR-U window doubled to 48 months. The Income Tax Act 2025 doesn't apply to your current filing — that's next year. For salaried income under ₹15 lakh, the new tax regime is now mathematically unbeatable. Read my full Old vs New Tax Regime 2026 salary comparison for the salary-by-salary breakdown.

What Changed for ITR Filing 2026 — The 7-Rule Cheat Sheet

If you're in a hurry, here's the full picture:

- ₹12 lakh income is now fully tax-free under the new regime (₹12.75L for salaried) — Section 87A rebate jumped from ₹25,000 to ₹60,000

- ITR-1 and ITR-2 deadline: July 31, 2026

- ITR-3 and ITR-4 deadline: August 31, 2026 (extended by a month for non-audit business and freelancers)

- HRA 50% exemption now applies to 8 cities — Bengaluru, Pune, Hyderabad, Ahmedabad newly added (old regime only)

- ITR-U window extended to 48 months (4 years) from the end of the assessment year

- You can now file ITR-U even after a reassessment notice — with immunity from under-reporting penalties

- Schedule AL threshold raised to ₹1 crore total income

Now let's actually break each one down with numbers, because vibes don't pay your tax bill.

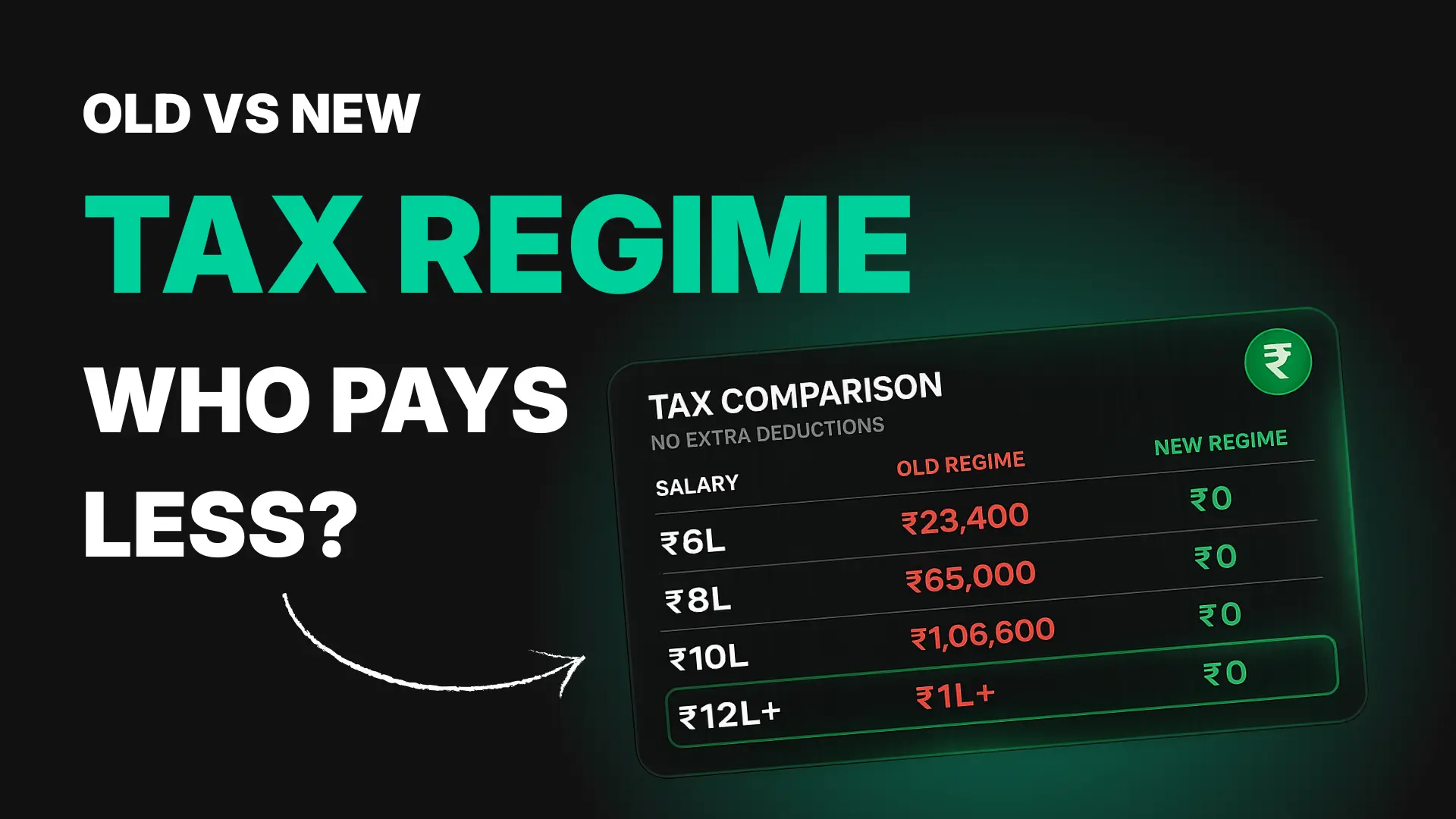

1. The ₹12 Lakh Tax-Free Bomb That Made the Old Regime Obsolete

This is the rule that quietly killed the old regime for most people, and somehow it's still being underplayed by mainstream finance media.

For FY 2025-26 (AY 2026-27), the Section 87A rebate under the new tax regime jumped from ₹25,000 to ₹60,000. Translation: if your taxable income is up to ₹12 lakh, you pay zero income tax. Period.

For salaried folks, it gets even better. The standard deduction of ₹75,000 stacks on top, which means your gross salary up to ₹12.75 lakh is effectively tax-free under the new regime.

Let me put this in real numbers I actually understand:

| Gross Salary | Old Regime Tax (with maxed deductions) | New Regime Tax | Winner |

|---|---|---|---|

| ₹6,00,000 | ₹0 (after rebate) | ₹0 | Tie |

| ₹9,00,000 | ₹35,000+ | ₹0 | New saves ₹35K+ |

| ₹12,00,000 | ₹95,000+ | ₹0 | New saves ₹95K+ |

| ₹12,75,000 | ₹1,05,000+ | ₹0 | New saves ₹1.05L+ |

| ₹15,00,000 | ₹1,40,000+ | ₹1,05,000 | New saves ₹35K |

| ₹20,00,000 | ₹2,80,000+ | ₹2,40,000 | New saves ₹40K |

Old regime calculations assume ₹1.5L 80C + ₹50K 80CCD(1B) + ₹25K 80D — basically a maxed-out tax saver. Most people don't even hit this.

Here's the spicy take nobody wants to say: for income under ₹15 lakh, the old regime now requires you to invest aggressively in tax-saving instruments just to match the new regime. That's not tax saving. That's tax-saving theatre.

The crossover point — where old regime actually beats new regime — kicks in around ₹15–18 lakh, and only if you have a home loan, full HRA exemption, and maxed 80C plus 80CCD(1B). For anyone earning under that, new regime wins on math alone.

For my own situation? I'm earning a mix of salary and freelance income. Even when I add my projected MonuMoney.in revenue to my day job salary, I'm sitting comfortably under ₹15L. The new regime is a no-brainer.

Critical catch — marginal relief at ₹12L–₹12.75L: If your income is ₹12,10,000, you don't suddenly pay ₹61,500 in tax. Marginal relief ensures you only pay tax equal to the income above ₹12L. So at ₹12.10L, your tax is roughly ₹10,000 — equal to the ₹10K extra income.

Run your own numbers using the Income Tax Calculator (Old vs New Regime) — it does the math for both regimes side by side.

2. Form-Specific Deadlines: Why Mix-Income Earners Got an Extra Month

This one is critical for anyone with mix income (like me).

The CBDT split ITR filing deadlines by form for AY 2026-27:

- ITR-1 (Sahaj): Salaried only, income up to ₹50 lakh — Deadline July 31, 2026

- ITR-2: Salaried + capital gains + multiple house properties — Deadline July 31, 2026

- ITR-3: Business or profession income — Deadline August 31, 2026 (non-audit)

- ITR-4 (Sugam): Presumptive income (44AD/44ADA freelancers) — Deadline August 31, 2026 (non-audit)

- Audit cases (any form): October 31, 2026

Why this matters: if you're a freelancer using Section 44ADA presumptive scheme (50% of gross receipts as taxable, no detailed books needed), you now get an extra month. That's significant when you're chasing client invoices and bank reconciliations.

For mix-income earners like me — salary + freelance — you'll likely use ITR-3 or ITR-4 depending on whether you opt for presumptive taxation. So my actual deadline is August 31, 2026, not July 31. A lot of CAs are still defaulting to the old "everyone files by July 31" mental model.

If you're running a small restaurant, kirana store, or any 44AD business, I'd strongly recommend reading my Budget 2026 Restaurant Tax Saving Guide using 44AD — it covers the exact presumptive math that most CAs underuse.

Spicy take: if your CA tells you that you have to file by July 31 because "that's the rule," and you have business or freelance income, get a second opinion. They might be panic-rushing your return for no reason.

3. The 8-City HRA Expansion Almost No Blog Has Covered Properly

This rule is wild because it's a genuine win for old regime filers, and it's buried in the new Income Tax Rules 2026.

Old rule: 50% HRA exemption applied only to 4 metros — Mumbai, Delhi, Chennai, Kolkata. All other cities got 40%.

New rule from April 1, 2026: 50% HRA exemption now applies to 8 cities — Mumbai, Delhi, Chennai, Kolkata + the newly added Bengaluru, Pune, Hyderabad, Ahmedabad.

Why this matters:

If you live in Bengaluru paying ₹35,000/month rent on a ₹12L basic salary, your HRA exemption just jumped from ₹1.96L (at 40%) to ₹2.45L (at 50%). That's roughly ₹49,000 of extra exemption per year.

But here's the catch I want everyone to read carefully: HRA exemption is still allowed only under the OLD tax regime. If you've already shifted to the new regime (which is the default), this rule doesn't apply to you.

So this rule is only useful if:

- You live in Bengaluru, Pune, Hyderabad, or Ahmedabad

- You're paying meaningful rent

- You're sticking with the old regime

- Your math actually works out better in old regime even with the higher tax slabs

For most middle-income earners in these cities, even with the new HRA expansion, the new regime's ₹12L rebate still wins. But for people earning ₹18L+ with high rent, the math now genuinely tilts back toward old regime. Run your own numbers — don't trust your CA's gut feel.

4. ITR-U: The 48-Month "Oops Window" That Just Got Massively Liberalised

This is one of those rules that doesn't matter until it absolutely matters.

Old rule: You could file an Updated Return (ITR-U) within 24 months from the end of the relevant assessment year, with additional tax of 25% or 50% depending on when you filed.

New rule for AY 2026-27: The ITR-U window has been extended to 48 months (4 years). And critically, you can now file ITR-U even after receiving a reassessment notice — which earlier was a hard stop.

Why this matters in real life:

Say you forgot to declare interest income from an old FD, or you missed reporting some freelance income from a foreign client that didn't show up in your AIS automatically. Earlier you had 24 months. Now you have 48 months to come clean.

Even better — filing ITR-U with the additional tax now provides immunity from penalties for under-reporting or misreporting. That's a big deal because under-reporting penalties can be up to 50% of the tax amount.

The catch: you'll pay additional tax on top of the original liability:

- Filed within 12 months: 25% additional

- Filed within 12–24 months: 50% additional

- Filed within 24–36 months: 60% additional (new tier)

- Filed within 36–48 months: 70% additional (new tier)

So yes, you have more time, but the longer you wait, the more it costs.

For freelancers especially, this is huge. Foreign clients pay in dollars, sometimes via wire, and that income occasionally slips through TDS reporting. Now you have 4 years to catch and fix it without facing a notice-driven penalty regime.

5. Schedule AL Threshold Raised to ₹1 Crore (Most Salaried Folks Just Got A Compliance Holiday)

Schedule AL is the form where you disclose your total Assets and Liabilities — your house, your cars, your bank balances, your gold, your stocks, your loans.

Old rule: Required if total income exceeded ₹50 lakh.

New rule for AY 2026-27: Required only if total income exceeds ₹1 crore.

If you're earning between ₹50 lakh and ₹1 crore, you no longer have to itemise every asset and liability you own when filing your ITR. That's a genuine compliance reduction for HNI-adjacent filers.

For most MonuMoney.in readers (the ₹6L–₹25L salary cohort I write for), this doesn't directly apply. But it signals where the IT department is heading: less compliance friction for the middle, more focus on the actual ultra-rich.

Honest take: I think this is a smart move. The earlier ₹50 lakh threshold caught a lot of people who were salary earners with maybe one apartment and some mutual fund holdings. Forcing them to itemise everything was bureaucratic theatre. ₹1 crore is a more meaningful threshold.

6. Pre-Filled Data Just Got More Aggressive (And You Need to Verify It Carefully)

The Income Tax Department's e-filing portal has expanded its pre-filled data. Now your ITR comes pre-loaded with:

- Salary (from Form 16 / employer TDS)

- Interest income (from bank AIS reporting)

- Capital gains (from broker AIS — Zerodha, Groww, Angel One, etc.)

- Dividend income (from listed companies)

- Foreign remittance details (LRS / Schedule FA)

Sounds like a feature, right? It's actually a trap if you don't verify.

The pre-filled data uses third-party reporting — banks, employers, brokers. They make mistakes. AIS shows wrong amounts surprisingly often. If you accept pre-filled data without cross-checking against your own bank statements and Form 26AS, you might:

- Pay tax on income you didn't actually earn (because of duplicate reporting)

- Miss income you DID earn (because some sources aren't covered by AIS)

- Get a notice for mismatch between AIS and your declared figures

My process this year: I'm downloading my AIS, my Form 26AS, AND every bank statement, and reconciling them line by line before I trust the pre-filled data. Tedious? Yes. Worth it? Absolutely. A notice will cost you 10x the time.

This is a textbook case of "trust but verify." The portal is helpful, but it's not a CA. It's automation built on third-party data feeds, and those feeds have errors. If you're tracking capital gains from mutual funds, the Mutual Fund Calculator on this site has an XIRR tab that gives you the actual annualised number to cross-check against your broker AIS.

7. The Income Tax Act 2025 Confusion — Don't Let It Throw You Off

Last one. This is the rule everyone is scared about and it actually doesn't apply to your AY 2026-27 filing yet.

The new Income Tax Act, 2025 came into effect on April 1, 2026, replacing the Income Tax Act, 1961. New section numbers (536 sections vs the old 819), new structure, new "Tax Year" terminology replacing "Previous Year + Assessment Year."

But here's the thing nobody is shouting loud enough:

The new Act applies to income earned in Tax Year 2026-27 (FY 2026-27) — which you'll file in 2027.

For your AY 2026-27 ITR (which covers FY 2025-26 income, the one you're filing right now between April–August 2026) — the OLD Income Tax Act, 1961 still applies in full. Old slabs, old deductions, old form numbers.

This transition has confused half the internet. Some blogs are screaming "FILING RULES CHANGED" and showing rates that don't apply for another year. Others are saying "nothing changed" and missing the genuine procedural updates that DID happen (the deadline split, the HRA expansion, the 87A rebate increase).

The reality: computation under old Act, but procedural compliance from April 2026 onwards (advance tax, TDS, etc.) follows the new Act framework. Your e-filing portal handles both simultaneously.

For your current ITR, just remember: old Act, new rebate, new HRA, new ITR-U window, new Schedule AL threshold. That's the practical reality.

My Personal Filing Strategy For AY 2026-27 (Mix-Income Earner)

Since I'm filing for the first time as someone with both salary and freelance income, here's exactly what I'm doing:

- Choosing ITR-3 because I have business/profession income from MonuMoney.in

- Going with the new tax regime — my combined income is well under ₹15L, so the ₹12.75L tax-free zone covers most of it

- Filing by August 31, 2026 (the extended deadline for non-audit ITR-3)

- Reconciling AIS, Form 26AS, and bank statements before trusting any pre-filled data

- Skipping Schedule AL because total income is well below ₹1 crore

- Keeping all client invoices and payment receipts for at least 6 years (the new ITR-U window plus buffer)

Will I switch to ITR-4 with Section 44ADA presumptive (50% of gross as taxable, no books needed)? Probably not yet — my freelance income is still small and irregular. ITR-3 with actual expense claims gives me cleaner numbers for now.

If you're in a similar situation, run your numbers through the Income Tax Calculator and check what your actual liability is under both regimes before you file anything.

What This Means For You — The Honest Bottom Line

If your taxable income is under ₹12 lakh and you're still planning to "save tax" by aggressively investing in 80C/80D/80CCD instruments under the old regime, you're probably wasting your money.

That doesn't mean don't invest. It means invest because the investment itself is good — long-term equity SIPs, PPF for safe long-term goals, NPS for the exclusive ₹50K under 80CCD(1B) if you're sticking with old regime — not because you need the tax deduction. The deduction was a nudge. The nudge worked when the alternative was paying ₹50K–₹95K of tax. Now that the alternative is ₹0 tax, the math has fundamentally changed.

For income between ₹12.75L and ₹18L, run the numbers carefully. Old regime might still win for you if you have HRA + home loan + maxed 80C + 80CCD(1B). For most people I know, it doesn't. I broke this down with side-by-side math in my Old vs New Tax Regime 2026 salary comparison — read that next if you're stuck on the regime choice.

Above ₹18L–₹20L, the comparison gets genuinely close and depends entirely on your specific deduction stack.

The 7 rules above aren't just compliance updates. They're a signal that the government has decided: simpler structure, lower nominal slabs, fewer deductions, more rebate at the bottom. The old regime was always a complex maze. The new regime is becoming the default for a reason.

File smart. Verify your AIS. Don't let outdated CA advice cost you money.

Frequently Asked Questions

Is income up to ₹12 lakh really tax-free for FY 2025-26?

Yes, under the new tax regime, resident individuals with taxable income up to ₹12 lakh pay zero tax due to the Section 87A rebate of ₹60,000. For salaried employees, the standard deduction of ₹75,000 raises the effective tax-free limit to ₹12.75 lakh. This applies for FY 2025-26 (AY 2026-27) returns being filed now.What is the last date to file ITR for AY 2026-27?

ITR-1 and ITR-2 deadline is July 31, 2026. ITR-3 and ITR-4 (non-audit cases) deadline is August 31, 2026. Audit cases have until October 31, 2026. Belated returns can be filed until December 31, 2026, but with late fees and interest charges.Can I still claim HRA in 2026?

Yes, but only under the old tax regime. The new tax regime does not allow HRA exemption. From AY 2026-27, the 50% HRA exemption applies to 8 cities including Bengaluru, Pune, Hyderabad, and Ahmedabad (in addition to the existing 4 metros — Mumbai, Delhi, Chennai, Kolkata).Is the new Income Tax Act, 2025 applicable for my current ITR filing?

No. For AY 2026-27 (income earned in FY 2025-26), the Income Tax Act, 1961 still applies in full. The new Income Tax Act, 2025 will only apply for Tax Year 2026-27 income, which you'll file in 2027. Don't let the noise about the new Act confuse your current filing.Which tax regime should I choose for ITR filing 2026?

For most salaried individuals with income up to ₹15 lakh, the new tax regime is mathematically better due to the ₹60,000 rebate under Section 87A. For income between ₹15L–₹18L, run both calculations carefully — old regime can win if you have HRA + home loan + maxed 80C + 80CCD(1B). Above ₹18L, it depends entirely on your specific deduction stack. Use the [Income Tax Calculator](https://monumoney.in/calculators/tax-calculator) to compare both for your exact numbers.How long do I have to file ITR-U for AY 2026-27?

Up to 48 months (4 years) from the end of the assessment year, i.e., until March 31, 2031. This is double the earlier 24-month window. Additional tax ranges from 25% to 70% depending on when you file within this window — 25% if filed within 12 months, 50% within 12–24 months, 60% within 24–36 months, 70% within 36–48 months.What if I miss the July 31 / August 31 deadline?

You can still file a belated return by December 31, 2026, but with a late filing fee of ₹5,000 (₹1,000 if total income is below ₹5 lakh) plus interest under Section 234A on any unpaid tax. More importantly, late filers cannot switch tax regimes — you'll be stuck with the new regime by default. If old regime works better for you, file on time.Disclaimer: This post is for informational purposes only. I am not a SEBI-registered investment advisor or a chartered accountant. Tax rules can change — always verify current rules at the official Income Tax Department website and the CBDT portal before filing. For specific tax situations, consult a qualified CA. Sources referenced: Income Tax Department of India, Central Board of Direct Taxes (CBDT), Ministry of Finance press releases.

Questions? Email me at contact@monumoney.in or find me on X @monu_money.

Official Sources & Verification

To ensure accuracy, the formulas, rules, and tax provisions used on this page are verified against official government, regulatory, or institutional sources.

- Income Tax Department of India

- Union Budget & Finance Bill

- Reserve Bank of India (RBI)

- Securities and Exchange Board of India (SEBI)

Last Verified: May 4, 2026